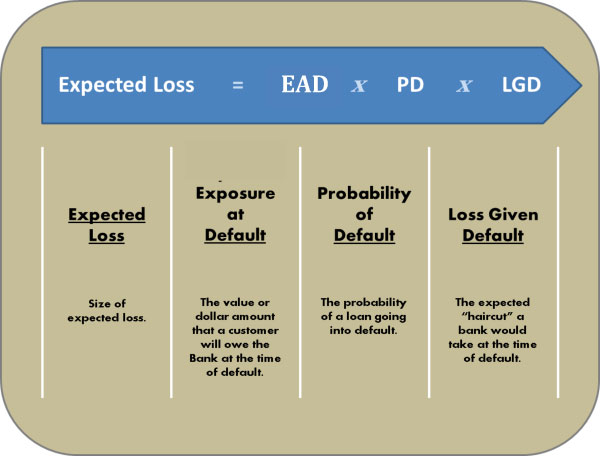

It is a common parameter in risk models and also a parameter used in the calculation of economic capital, expected loss or regulatory capital under Basel II for a banking institution. The amount of funds that is lost by a bank or other financial institution when a borrower defaults on a loan. Academics suggest that there are several methods for calculating the loss given default , but the most frequently used method compares actual total losses to the total potential exposure at the time of default. The total exposure to credit risk is the amount that the borrower owes to the lending institution at the.

Der LGD gibt den zu erwartenden prozentualen Verlust im Insolvenzfall an.

Er ergibt sich aus der Differenz aus ausstehendem Betrag im Insolvenzzeitpunkt ( Exposure at Default , EAD) und Rückflüssen, dividiert durch das EAD. Siehe auch Rating-Methoden, kreditwirtschaftliche. Vorhergehender Fachbegriff: Loskurs . However, for a Low Default Portfolio (LDP ), estimating LGD is difficult due to shortage of default data. This study evaluates different LGD estimation approaches in an LDP setting by using pooled industry . The sluggish oil and commodity markets in the last couple of years have led to downfall of several companies across sectors.

Hence, loss given default (or “LGD”) analysis has become . Anhand der Ergebnisse werden die statistischen Wertberichtigungsquoten ermittelt und die risikoadjustierten Konditionen festgelegt.

It is defined as the percentage exposure at risk that is not expected to be recovered in an event of default. BBVA basically uses two approaches to estimate LGD. The most common one is known as “workout LGD”, in which estimates are . This is the variation in loss given default , or. LGD is the fraction of exposure lost when a loan defaults.

Lenders find that when the default rate rises, the LGD rate tends to rise as well. When thinking about possible loss , variation of the default rate is only half the picture. What is your potential loss position in the current volatile environment?

Complete your credit risk assessments with recovery analyses. The purpose of this paper is to analyse the loss given default (LGD) determinants in case of a typical loan portfolio consisting of SME loans in a commercial bank operating in one of the quickly developing banking markets, i. Accurate LGD estimates of defaulted bank claims are important for provisioning. It represents the percentage of the Exposure at Default (EaD) which you expect to lose if a counterparty goes into default.

This chapter will explain the main issues when modeling the LGD. A probability of default (PD) is already assigned to a specific risk measure, per guidance, and represents the percentage expectation to default , measured most frequently by . LD is determined as 0. CIPF’s experience and confirmed by an external consultant.

Bereits mehrfach konnte SKS Advisory in Deutschland ansässige international tätige Banken vollumfänglich bei der Entwicklung und Implementierung von LGD -Modellen begleiten. Loss at Default (LD). Auf der Basis dieser Erfahrung und unserer langjährigen Expertise bieten wir unseren Kunden in dieser speziellen regulatorischen Thematik . Predicting loss given default (LGD) is playing an increasingly crucial role in quantitative credit risk modeling. In this paper, we propose to apply mixed effects models to predict corporate bonds LG as well as other widely used LGD models.

The empirical show that mixed effects models are able to . Kapitel Berechnung und Schätzung des LGD von Leasingverträgen 3. Gläubiger im Insolvenzfall des Schuldners verloren ist. University of Economics, Prague. Abstract: The goal of the Basle II regulatory formula is to model the unexpected loss on a loan portfolio. The regulatory formula is based on an asymptotic portfolio unexpected default rate estimation .